What you’ll learn in this article…

- Tax-free employer tuition aid capped at $5,250 under IRS 127.

- Chamberlain-Advocate Health partnership trades tuition for work commitments.

- Median RN salary of $86,070 offsets multiyear work obligations.

Employer-tied loan assistance is shifting from a niche perk to a mainstream pipeline for BSN students. The Chamberlain University and Advocate Health partnership offers loan help in exchange for a post-graduation work contract, mirroring deals at health systems aiming to fill staffing gaps. For nursing students, the offer pairs immediate financial relief with a binding obligation that can restrict specialty choice and geographic mobility. As more hospitals adopt these models, understanding the long-term career cost of a signed contract becomes as critical as the dollar amount of tuition covered. This guide walks through how these programs work, what the fine print actually says, and how to weigh financial relief against the career flexibility you may be giving up.

How Employer-Sponsored BSN Programs Work

Employer-sponsored BSN programs aren't one-size-fits-all: the way money moves, who pays when, and what you owe in return vary dramatically across four distinct models. Understanding how cash flows in each can mean the difference between a smart financial move and a career-limiting commitment.

How the Money Flows: Four Distinct Models

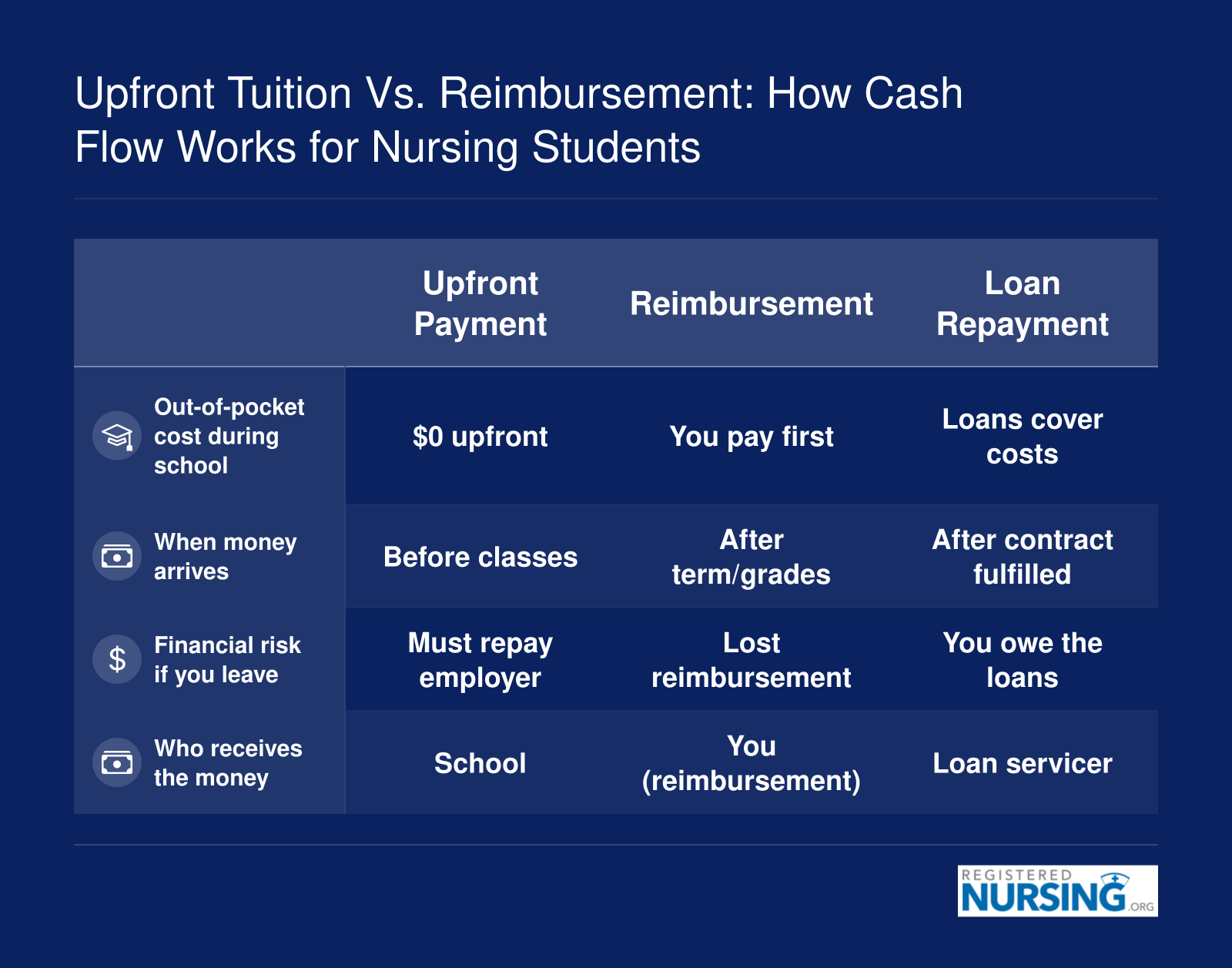

- Upfront Tuition Payment: The employer pays your school directly before or during each term. You may need to maintain a minimum GPA, but you avoid out-of-pocket costs entirely. Forgivable tuition assistance , where the debt is cancelled after you complete a service obligation , falls under this umbrella.

- Tuition Reimbursement: You pay tuition when it's due, often per course, and submit grades or receipts afterward. The employer reimburses you, typically up to an annual cap and only for courses with a C or better. This model requires upfront cash or short-term loans.

- Loan Repayment Assistance: You take out federal or private loans to fund your BSN, finish the program, and then the employer makes loan payments on your behalf, usually after you start working. You carry the debt during school, but the employer lightens the load once you're on payroll.

- Pipeline Partnerships: A structured agreement between an employer and a nursing school that bundles scholarship, clinical placement, loan repayment, and a guaranteed employment pathway. You commit to work for the employer after graduation in exchange for financial support that flows across your program.

A Pipeline in Practice: Chamberlain and Advocate Health

The Chamberlain University, Advocate Health pipeline illustrates this last model clearly.1 The program offers BSN students a dedicated Acute and Progressive Care nursing pathway, with scholarship funds, clinical placements at Advocate Health facilities, loan repayment, and a direct employment pathway , all in exchange for a post-graduation work commitment at Advocate Health. The program launches each September, targeting students who want a seamless transition from classroom to bedside. It's a textbook example of how a large health system uses financial relief as both a recruitment and retention lever, reducing student debt while locking in a future nursing workforce.

Online, Hybrid, and Campus-Based: What Employers Cover

Availability varies by format. Historically, many employer-sponsored programs only covered campus-based BSNs, but that's changing. LCMC Health's Called-to-Care Scholars Program, for instance, provides forgivable tuition assistance for campus-based students and requires non-Louisiana residents to relocate.2 Meanwhile, SSM Health's Aspiring Nurse Program supports a fully online BSN through a loan-repayment model: you take out loans, complete your coursework online, and SSM Health repays those loans over a four-year service term.3 Chamberlain's partnership with Advocate Health reflects the increasing flexibility; Chamberlain offers online and hybrid BSN options, and MSN scholarships, grants, and loan forgiveness illustrates how financing strategies are evolving beyond employer pipelines as the demand for remote learning grows.

Why the Push? The Workforce Gap Meets Recruitment Strategy

These programs are expanding because nursing shortages leave health systems scrambling. Employer-funded BSN paths serve as powerful hiring tools, binding new graduates to a system for several years while easing the financial burden that often deters prospective nurses. Across the country, large systems , from HCA Healthcare to Kaiser Permanente , have launched their own versions of tuition support, signaling that employer-sponsored BSNs are shifting from a niche perk to a standard recruitment strategy. For nursing students, the choice isn't simply about getting help with loans; it's about deciding which financial model and which career trade-off fits your long-term goals.

What's Typically in a BSN Work Contract? Key Terms to Review

Some employer programs cover tuition upfront with no strings attached; others require you to trade a post-graduation work commitment for that financial help. If you're weighing an employer-sponsored BSN, understanding what's buried in the fine print is just as important as knowing how much tuition they'll pay.

Service Commitment Length: 2-4 Years Is Common

Once you accept tuition assistance, most hospitals or health systems want a return on their investment. The standard service commitment ranges from one to three years after you complete your degree or after each year of funding, depending on the program.1 HCA, for example, typically requires a three-year commitment for nursing education benefits.1 Mercy Southeast structures it as one year of service for each year they provide tuition assistance, up to three years.2 Shorter commitments (12-18 months) are less common but do exist, especially for smaller amounts or internal pipeline programs. Always confirm whether the clock starts ticking after graduation, after your last reimbursed course, or after you pass the NCLEX.

Repayment Clauses: What Happens If You Leave Early?

The repayment terms are the contract's sharpest edge. Most agreements use a prorated clawback: the amount you owe decreases based on how much of the commitment you've worked.3 If you leave after one year of a three-year agreement, you might owe roughly two-thirds of the total assistance received. Some contracts, however, demand full repayment if you exit before hitting a minimum threshold, say, before completing 12 months. The repayment is often structured as a promissory note that becomes a collectible debt.1 Before signing, ask for a clear, written illustration: "If I leave after 18 months, exactly how much would I owe?" Don't rely on verbal assurances.

GPA and Enrollment Requirements

Employers aren't just funding your degree; they're investing in a future nurse who can meet licensing and clinical standards. Many programs set a minimum GPA, typically 2.0 to 2.5, and tie reimbursement percentages to grades.4 A common tiered model pays 100% for an A, 75% for a B, and 50% for a C.4 You may also need to maintain continuous enrollment, not drop below a certain credit load, and submit grades or transcripts promptly. Missing a semester or falling below the GPA floor can void your funding or trigger early repayment, even if you haven't graduated.

Probationary Periods and Location Restrictions

Before you're eligible for any tuition benefit, most employers impose a probationary employment period, often 90 days to one year from your hire date.5 So if you start a job thinking you'll immediately get tuition help, you may need to wait. Additionally, contracts frequently restrict where you can work during and after the commitment. You might be required to work in a specific facility, unit, or geographic region and may not be able to transfer to a different hospital within the same system without permission. These location locks can limit your options if a better opportunity arises across town.

The Legal Landscape: TRAPs and Regulatory Scrutiny

Training repayment agreement provisions (TRAPs) are facing increasing legal pushback. The Federal Trade Commission proposed a rule in 2023 to ban non-compete clauses, and advocacy groups argue that many TRAPs function as de facto non-competes for nurses. Several states have already restricted or banned training repayment agreements, particularly when they saddle workers with high debt for low-wage jobs. While nursing residencies and internships sometimes include similar service-commitment language, the broader regulatory environment is shifting. Nurses considering a BSN work contract should monitor this evolving legal area , a contract signed today could be subject to new state laws tomorrow.

Questions to Ask Yourself

Upfront Tuition Vs. Reimbursement: How Cash Flow Works for Nursing Students

Employer-sponsored BSN programs fit into three common structures: upfront payments, reimbursement models, and loan repayment assistance. Each approach affects your cash flow differently during school and your financial risk if you leave the employer early.

Tax Implications of BSN Tuition Reimbursement

How much of my employer-paid BSN tuition will be taxed?

Understand the IRS Section 127 rules before you count on full financial relief. Employers can provide up to $5,250 per year in educational assistance tax-free.1 Any amount above that threshold is considered taxable income and will appear on your W-2, reducing your net pay just as a bonus would. For nursing students considering a work contract for BSN loan help, knowing exactly how much of that benefit hits your tax return is essential.

The Section 127 Cap: $5,250 Tax-Free

Under Section 127 of the Internal Revenue Code, employers may reimburse tuition, fees, books, and supplies up to $5,250 per calendar year without those dollars counting as gross income for the employee.1 This cap has held steady at $5,250 for several years and is not indexed for inflation until 2027.2 That means for the 2026 tax year, the same $5,250 limit applies. If your BSN program costs $15,000 per year and your employer covers all of it, roughly $9,750 becomes taxable. Between federal income tax, state tax (where applicable), and FICA, you could see several thousand dollars withheld from your paychecks over the year, effectively reducing the "free" money you thought you were getting.

What Counts Above the Cap

The employer must report any reimbursements above the $5,250 exclusion on your W-2 as wages. You pay ordinary income tax on that amount, plus Social Security and Medicare taxes.3 It is not treated as a separate fringe benefit with a flat rate; it stacks on top of your regular salary. If you are in a higher tax bracket, the bite is larger. Some employers try to structure assistance as a working condition fringe benefit, for instance arguing the education maintains or improves skills needed for your current job, but typical BSN degrees for pre-licensure students rarely qualify under that narrow exception.4 Most nursing tuition programs fall squarely under Section 127, and the excess is simply taxable.

Student Loan Repayment: Permanent, but with Limits

A popular provision from the CARES Act allowed employers to make tax-free student loan payments up to $5,250 through 2025. That temporary window has closed. However, the SECURE 2.0 Act made employer-paid student loan repayment permanently tax-free under Section 127, effective for payments made after 2023.1 Starting in 2024 and continuing through 2026 and beyond, the same $5,250 cap applies. Importantly, the cap is a combined total: if your employer pays $3,000 toward your BSN tuition and $3,000 toward your existing student loans in the same year, only $5,250 is excluded.3 The extra $750 becomes taxable wages. So, a contract that promises both tuition reimbursement and loan assistance might leave you with an unexpected tax bill if the total exceeds the annual threshold.

Before You Sign: Get the Numbers in Writing

Ask human resources for a clear, written breakdown of which portions of the educational benefit are taxable and which are tax-free. Request the projected W-2 impact if possible. Some employers cover the employee's tax liability through a "gross-up" payment, but that is rare in nursing pipeline programs. If gross-up isn't offered, run the numbers yourself: multiply the taxable excess by your marginal tax rate (federal + state) and add 7.65% for FICA to estimate the after-tax cost of the "free" tuition. For a $15,000 benefit, a nurse in the 22% federal bracket with a 5% state tax might pay roughly $4,338 in additional taxes, making the net value of the benefit around $10,662 instead of $15,000. Knowing that figure ahead of time helps you decide whether the contract is worth signing. If you are also weighing other funding options, cheapest nurse practitioner programs are worth comparing against employer-tied arrangements before you commit.

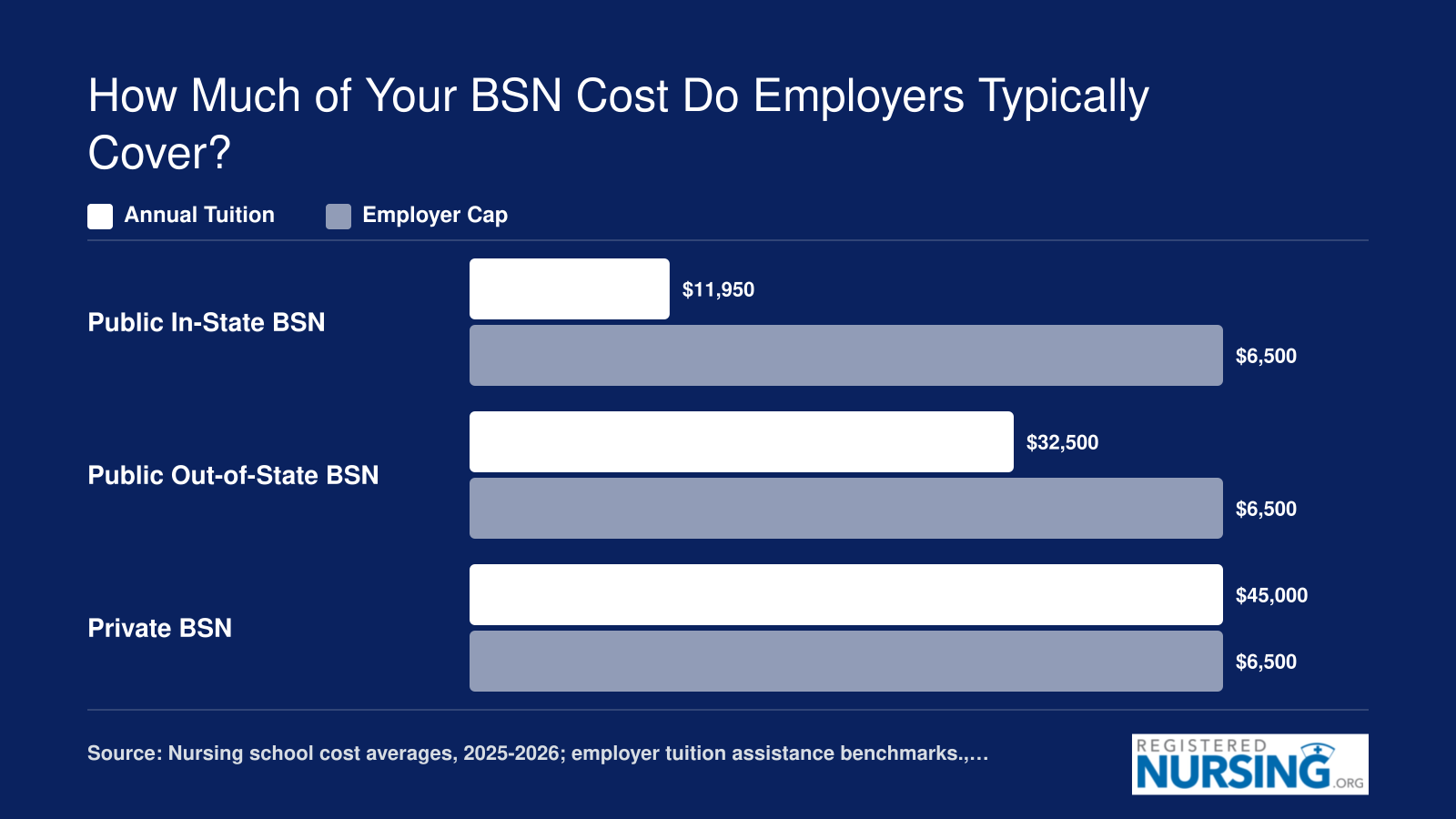

How Much of Your BSN Cost Do Employers Typically Cover?

A typical BSN costs $11,950 per year at a public in-state college and up to $45,000 at a private institution, while most employer reimbursement plans cap annual contributions at $3,000 to $10,000. Pipeline partnerships like the Chamberlain-Advocate Health program may cover a larger share, but general reimbursement often leaves students covering 50% or more of their total costs.

Related Articles

Career Trade-Offs: Financial Relief Vs. Mobility and Specialty Choice

The appeal of tuition help signed away with a single signature can feel immediate, but the long-term career map requires a closer look. An employer-backed BSN program trades a few years of free or reduced tuition for a lock on where and how you practice nursing. Two paths unfold: one where debt shrinks with each paycheck and another where professional flexibility pays its own dividends. The choice hinges on which future you are designing.

When You Pin Yourself to One Map

A two- to four-year work commitment after graduation ties your license to a specific facility or health system. That anchor can complicate relocation for family, a spouse's career, or personal preference. Breaking the contract often means repaying the full tuition amount, sometimes with interest or penalties, turning a financial lifeline into a sudden debt. Even a transfer within the same health system may not count if your agreement specifies a particular campus or unit.

Specialty Tracks and the Timing Trap

Advanced practice roles rarely follow a straight line. Nurse practitioner tracks, CRNA programs, and nursing informatics programs often demand experience in varied clinical environments. A contract that requires two years of medical-surgical nursing at one hospital can delay your application timeline or narrow your exposure to the critical care hours CRNA schools expect. If your employer does not house the specialty unit you need, you may watch a cohort of peers advance while you wait out your obligation.

- NP programs: Most require recent, relevant bedside experience. If your contract locks you into a non-specialty floor, you may need extra time post-contract to build the right case for admission.

- CRNA tracks: High-acuity ICU experience is nearly mandatory. A contract that cannot guarantee that assignment becomes a barrier.

- Nursing informatics: Roles often emerge in health systems with mature technology departments; a small community hospital may never open that door.

Employer Contracts vs. Federal Loan Forgiveness

Federal Public Service Loan Forgiveness (PSLF) offers a contrasting path. Instead of committing to a single employer, you work ten years at any qualifying nonprofit or government facility. This preserves mobility: you can change hospitals, move across state lines, or shift into school nursing without losing progress. The trade-off is time, a decade of service versus a two-year contract. For nurses weighing advanced education, however, that decade may overlap with graduate school and early career years, making PSLF a smoother fit for those who want to keep options open.

- Employer contract: Short commitment (2-4 years), high immediate relief, but low mobility.

- PSLF: Long commitment (10 years), slower forgiveness, but full employer and geographic flexibility.

Who Benefits Most from Signing?

Employer sponsorship works best when three conditions align: you trust the health system's culture, you plan to stay in the area, and your ideal first role is a generalist bedside position. For the student who sees a long future with one hospital, perhaps because of family roots or a strong clinical ladder, the contract cuts a clear path to a debt-free start. For everyone else, the fine print may cost more than tuition. Nurses drawn toward accelerated MSN programs or other advanced degrees will want to weigh whether a contractual commitment leaves enough room to pursue those goals on their preferred timeline.

Signing a work contract locks you in, but remember what's on the other side: the national median RN salary hovers near $86,070 annually (BLS 2024). Over a two-to-four year commitment, that's a solid foundation. Just know the math shifts by location. In high-wage states like California or Massachusetts, you'll earn well above that median; in lower-cost regions, the trade-off may feel steeper. Factor your local RN pay into the decision.

Checklist: Questions to Ask Before Signing an Employer BSN Contract

Before you commit, ask these critical questions to understand what you're agreeing to and what happens if your plans change.

- How long is the service commitment, and when does it start?Clarify whether the obligation period begins after graduation or when you start work as an RN. Some contracts start the clock on your first day of employment, while others count from the date of licensure.

- Is repayment prorated if I leave early?Ask if the amount owed decreases over time (e.g., you owe 100% if you leave within one year, 50% after two) or if you're liable for the entire sum regardless of how long you stayed.

- What academic or program requirements must I maintain?Many programs require a minimum GPA (often 2.5–3.0) and full-time enrollment. Missing a threshold or failing a course could cause immediate loss of benefits and trigger repayment.

- Can I choose my unit, facility, or shift?Some contracts tie you to a specific hospital, unit, or geographic region. Determine if you can transfer within the system or if you must accept whatever opening is available.

- How is the tuition benefit taxed?Under IRS Section 127, up to $5,250 per year in employer-provided tuition assistance may be tax-free. Amounts above that are generally taxable as income. Ask how the benefit will appear on your paycheck.

- Does the program cover online or hybrid BSN formats?If you're enrolled in a flexible program like an online or hybrid BSN, verify that the employer's reimbursement terms apply. Some only cover traditional, in-person programs.

- What happens if I'm laid off or the unit closes?Read the contract for termination clauses. If the employer eliminates your position or you're terminated without cause, you may still be on the hook for repayment. Request a waiver or prorated forgiveness for these scenarios.

Common Questions About Employer-Sponsored BSN Programs

Before signing a work contract for BSN tuition help, it is crucial to understand the legal, financial, and career implications. These frequently asked questions break down what you need to know.

- Will employers pay for my BSN degree?

- Yes, many hospitals and health systems offer tuition reimbursement or upfront payment for BSN degrees. Programs vary: some cover full tuition, others a percentage or capped amount. In exchange, you typically commit to working for the employer for a set period, often two to three years. Always review contract terms to understand coverage limits and repayment obligations.

- What happens if you break an employer tuition reimbursement contract?

- Breaking the contract usually triggers a repayment clause, requiring you to pay back some or all of the tuition assistance. These training repayment agreement provisions (TRAPs) can lead to debts of $10,000 to $30,000 sent to collections, damaging your credit. Enforceability varies: California banned such contracts for nurses in 2026, and Colorado restricts them. Consult a legal expert if you need to leave.

- How long do you have to work for an employer after they pay for your BSN?

- Typical work commitments range from two to three years after graduation or after receiving funds. The exact duration is specified in the contract and may vary by employer. If you leave before fulfilling the term, you may owe a prorated or full repayment. Make sure you are comfortable committing to the employer and location for that length of time.

- Is employer tuition reimbursement for nursing school taxable?

- Under current IRS rules, up to $5,250 per year in employer-provided educational assistance can be excluded from taxable income. Any amount above that threshold is typically treated as taxable wages. Some programs structure payments as working condition fringe benefits, which may also be tax-free. Check with a tax professional to understand your specific situation.

- Are employer-sponsored BSN programs worth it compared to federal loan forgiveness (PSLF)?

- It depends on your career goals. Employer-sponsored programs provide immediate financial relief but lock you into one employer, potentially limiting specialty changes or relocation. Public Service Loan Forgiveness (PSLF) requires 10 years of qualifying payments while working for a nonprofit or government employer, offering flexibility to switch jobs within those sectors. If you value early career mobility, PSLF may be more suitable.

- What is the Chamberlain Advocate Health nurse pipeline program?

- It is a partnership that offers loan assistance to BSN students enrolled at Chamberlain University in exchange for a work commitment at Advocate Health after graduation. The program aims to ease the nursing workforce shortage by reducing student debt while ensuring a pipeline of new nurses for the health system. It exemplifies the growing trend of employer-tied tuition assistance in nursing education.